While the backdrop for the Chinese consumer remains challenging, with little recovery in residential housing and stagnant retail sales growth, there have been some bright spots. One of these is travel, and in particular the hotel industry. The recent inflection in hotel pricing is positive for our investment in online travel agent, Trip.com, and has supported a new investment in the Chinese hotel chain, H World.

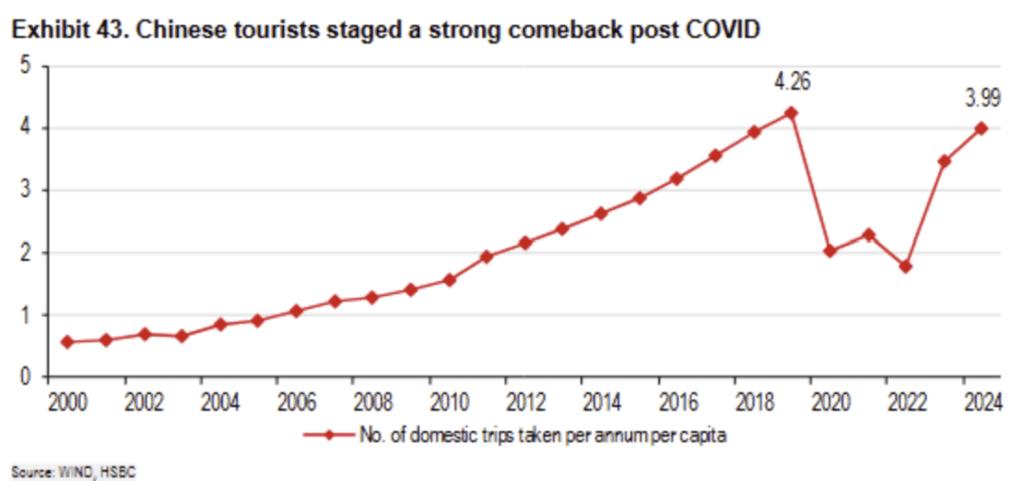

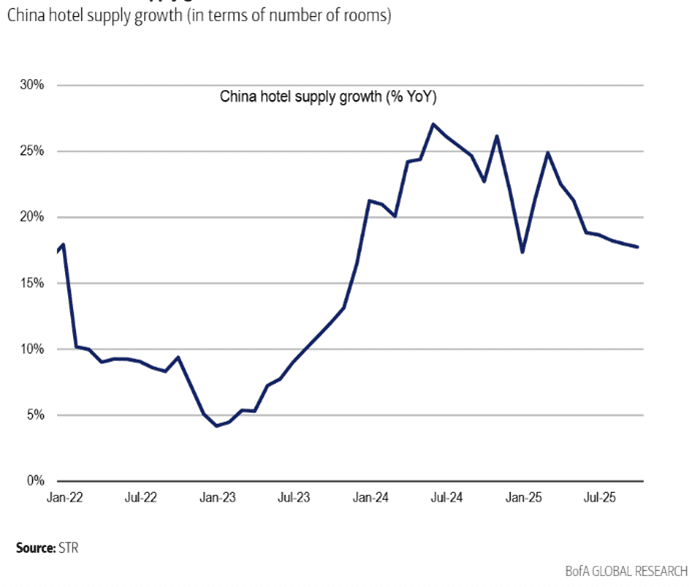

Chinese travel has been in a structural growth trend for most of the past two decades. The country’s COVID restrictions depressed travel for multiple years, but demand rebounded quickly once restrictions were lifted. While this was positive for demand, it was accompanied by a significant acceleration in hotel supply, which created a negative pricing dynamic over the past couple of years. The increase in supply was a response to the positive long-term outlook for travel demand combined with a downbeat equity market and a stagnant residential housing market, which forced investors to look elsewhere.

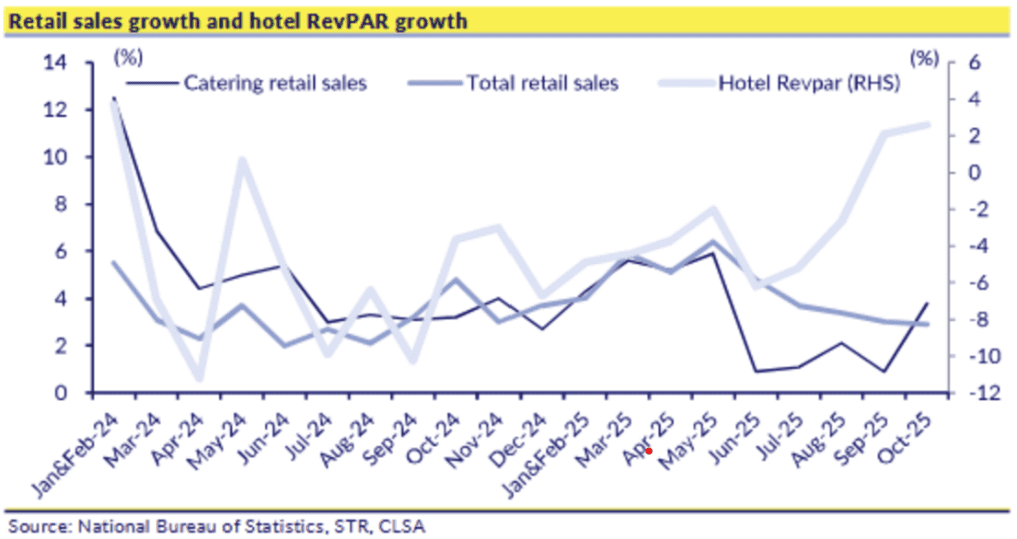

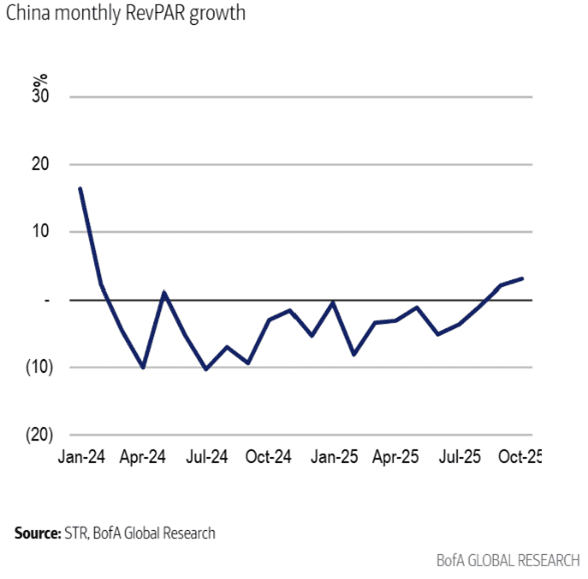

However, supply growth has started to decelerate, while demand remains resilient, resulting in hotel revenue per available room finally returning to positive growth. This is positive for Trip.com, which derives a significant portion of its profitability from domestic hotel bookings, and even more so for H World, which is the second-largest hotel chain in China.

The inflection in hotel pricing is certainly positive for short-term earnings growth and investor sentiment. However, the long-term opportunity for H World is also compelling.

Chains only account for ~40% of the hotel industry in China, versus over 70% in the U.S., so there is significant potential for growth. Furthermore, H World’s management sees an opportunity to become the leading consolidator in China’s fragmented hotel industry. H World targets a 15% market share in China’s chain hotel industry by 2030 and aspires to reach 40-50% market share, from less than 10% today.

Beyond growth in hotels and market share, H World is also focused on increasing its share of revenue from franchised and managed hotels. This asset-light expansion should help reduce earnings volatility and enhance cash flow generation. Ultimately, this should lead to greater returns to shareholders, with management already committed to a three-year capital return programme, which will involve a $2bn share buyback.

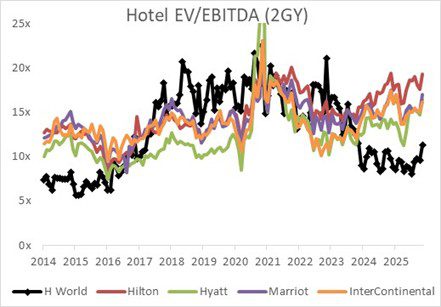

The improvement in Chinese hotel pricing has led to stronger short-term share price momentum for H World. However, valuation multiples remain low relative to history and low relative to U.S. hotel peers, suggesting there is still significant long-term upside potential.

Read our latest insight: “One of the few bright spots in Chinese consumption” – click here to view the full PDF