With President Trump in China this week the above subject is worth reconsidering.

Back in 2021 I visited the US to talk about Emerging Markets investment. Despite the strong year that China had had in 2020, the investors I met were not favourably disposed to the country with the biggest weighting in the EM index. Beijing was in the midst of clipping the wings of the entrepreneurial private sector. One investor* shut down my presentation by opining that “Xi is bombing that country back to the Cultural Revolution”. Another* by calling it “uninvestible”.

The concept of EM ex-China has ebbed and flowed in allocators’ minds since that time. There has certainly been a political tailwind to this dynamic. Another allocator let me know how one of his pensioners stopped him in the street and told him in no uncertain fashion that he hoped he wasn’t giving any of his hard earned savings “to those Chinese fellas”*.

As you know there has been a certain amount of state legislation that has prohibited investment in China.

Ignoring the political motivations for a moment and instead looking at the investment side of the argument, what do we see? Whilst China has been a happy hunting ground for investors in a number of years, there is little doubt that overall it has been hard yards across the last 20 years. Periods of clover followed by scorched earth caused by largely unpredictable factors.

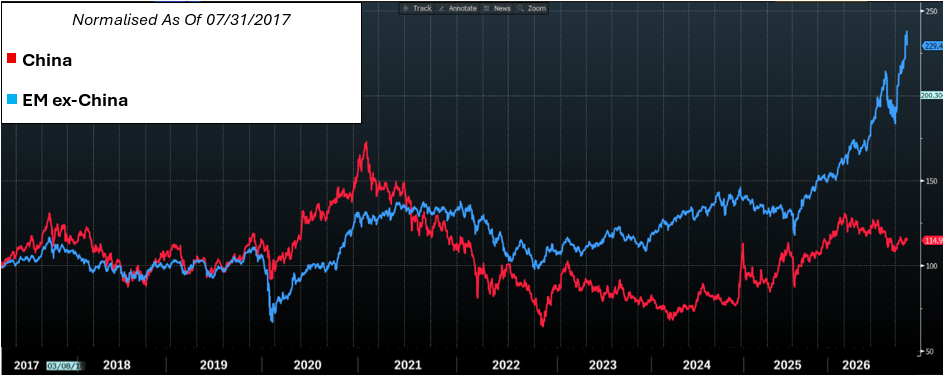

China and EM ex-China Since 2017

Source: Bloomberg

As the chart above illustrates whilst China and EM ex-China have produced comparable returns between 2011 and 2022 their paths over the last years have been divergent to say the least.

Having benefitted from tech sector excitement and market reforms in the 2010s, China’s performance since 2021 has been pedestrian, perking up in 2025 when DeepSeek popped up only to return to more dreary returns a few months later. The parlous state of the property market and geopolitical tensions as well as the back to the future policies alluded to above all played a part. Given its weighting in the EM index this is significant particularly as other EM markets have done some decent things in the interim. Since the end of 2021 in USD,

the MSCI China Index is up 2.5% vs. the MSCI EM ex-China Index has risen 72.2%. Annualised that is less than 1% compared to 13%.

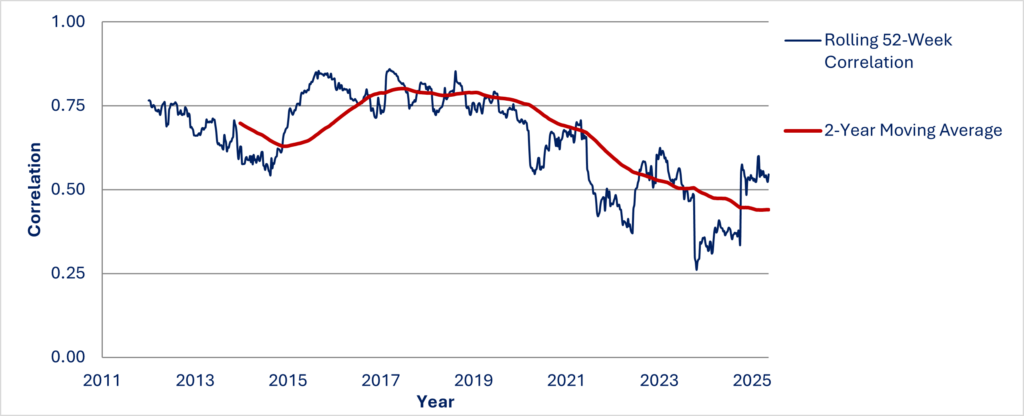

Many of you will be unsurprised that the correlation between China and EM ex-China has fallen over this period given the difference in the drivers that determine the very different economies that are lumped together as EM. Health policies pursued during Covid perhaps provided a catalyst for this decline.

Rolling 52-Week Correlation & 2-Year Moving Average: MSCI China vs MSCI EM ex China

Source: MSCI, Aubrey

There is further analysis discussing whether adopting an EM ex-China approach with a separate China allocation is the way to go which goes further than just the political. It does assume however that hard pressed allocators have the resource for pursuing such a strategy**. I suppose it is also open to argument that this reduction in correlation is merely cyclical rather than secular in nature and may simply be reversed by a flick of the pen in Beijing.

In the interests of transparency, we manage a EM ex China strategy. However, if the above sparks an interest, we would be delighted to discuss the above further.

*my thanks to Jeff, Kaz and Chris – your candour was, as ever, appreciated

**MSCI

Click here to view the PDF for ‘EM ex-China as an asset class – political or investment driven?’