‘’Ads plus AI is sort of uniquely unsettling to me. I kind of think of ads as a last resort for us for a business model’’

Sam Altman, May 2024

It’s no secret that OpenAI has bills to pay. Several high-profile deals with Oracle ($300bn), Microsoft ($250bn) and Broadcom ($350bn), among others, amount to over $1tn of commitments across varying time horizons. While the growth of ChatGPT has been exponential, its ability to fund this has come into question in the investment community, and now seemingly within OpenAI itself. Having declared a ‘Code Red’ following the release of Google’s Gemini 3 model last year, ChatGPT has started running ads in a move that Sam Altman himself previously labelled a last resort. The question is whether this attempt at monetisation is coming from a position of strength or weakness.

A key part of this shift has been the realisation that monetising consumers through a subscription model is proving harder than expected. While uptake has been rapid for ChatGPT, data suggests that it is still struggling to become a day-to-day part of people’s lives. The latest daily and weekly active user figures suggest engagement, based on daily and weekly active users (DAU/WAU), remains relatively low at 22%. For reference, apps such as Instagram are typically north of 50%.

Source: OpenAI public announcements and SensorTower

Source: OpenAI public announcements and SensorTower

This is also reflected in the relatively low levels of paid conversion to the premium tiers, with 3.7% of WAUs converting to premium subscriptions (Jan 2026) versus ~5% at the end of 2024. While 3.7% is not bad in isolation, it does not appear sufficient to justify the levels of investment. Improvements to the model and new features should be driving greater conversion of the user base rather than less. This challenge was acknowledged publicly on X by Sam Altman himself: ‘It is clear to us that a lot of people want to use a lot of AI and don’t want to pay.’

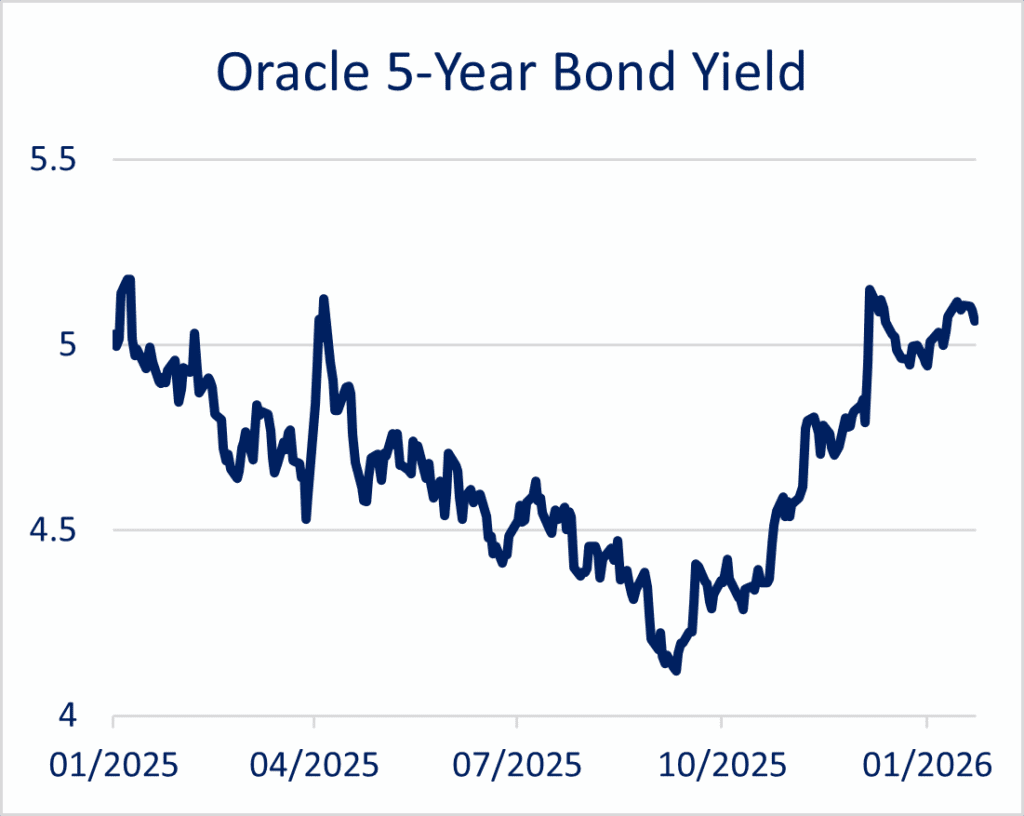

The consequences of these troubles are well documented. Oracle’s bond yield has increased significantly, and its share price has halved, as its debt raising to fund data centre infrastructure for OpenAI has begun to ring alarm bells. It is worth noting that its promise to raise ‘only’ $50bn this year has also failed to halt its slide. Microsoft has also taken a beating, with 45% of its backlog attributed to OpenAI, in a similar vein to Oracle.

Source: Bloomberg

Source: Bloomberg

Doubts over its ability to meet these commitments are clearly starting to weigh on investor sentiment, and OpenAI’s $1tn+ of commitments now look like a bigger number than they did even six months ago, particularly with a still uncertain ROI.

However, what looks underappreciated is the broader impact across the ‘picks and shovels’ space, which has been a huge source of performance over the past two to three years. While Microsoft and Oracle have borne the brunt, both companies are supplied by a huge ecosystem of AI-adjacent companies. For example, Nvidia is a leading supplier to Microsoft, Oracle and Amazon, which together hold over $600bn of cloud infrastructure commitments, putting a spotlight on their future pipeline should OpenAI begin to fall behind. Microsoft alone accounts for ~19% of Nvidia’s revenue.

In effect, OpenAI has become the marginal buyer of high-end AI compute. Any slowdown in its ability to fund or monetise that demand would therefore transmit rapidly through hyperscalers and into the semiconductor supply chain.

Further up the supply chain on the hardware side, familiar names such as SK Hynix, Micron, TSMC, KLA and ASML are all key suppliers to a further ~$550bn of commitments to Nvidia, Broadcom and AMD. Many of these names continue to perform very well, reflecting extraordinarily little of the risk that appears inherently priced into Microsoft and Oracle. OpenAI’s upcoming IPO in either late 2026 or early 2027 should help to alleviate some of the funding concerns. It will also provide an interesting barometer for the sustainability of the AI trade.

Talk of an AI bubble seemingly disappeared at the beginning of 2026, supported by further commitments from Meta and Microsoft to increase capex forecasts beyond all expectations. We do not view this commitment as likely to change but are concerned about the prospect of OpenAI overextending itself and the impact this could have. We have reduced or avoided the names most exposed to OpenAI’s supply chain and will continue to do so until we see sufficient upside to their performance. Given OpenAI’s importance to the overall AI narrative, failure to sufficiently monetise

its new advertising venture begins to look like a key catalyst that could turn talk of a bubble into reality. We remain selective and underweight U.S. technology companies, and continue to urge investors to remain cautious about extending their exposure to the broader AI supply chain.

A PDF of “OpenAI – The Beginning of the End?” is available here.