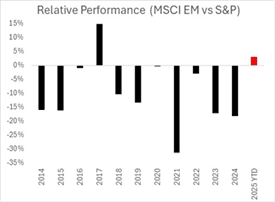

US exceptionalism has kept the party humming. Suggestions that diversifying away from the S&P on valuation alone have been repeatedly confounded. Emerging Markets have been cheaper whilst offering decent prospects and yet have underperformed since 2017. In that time they have just got steadily cheaper relative to the S&P 500 for a number of years with relative PE now close to 0.55x.

Source: Aubrey Capital (Bloomberg) 28 February 2025

And this at the same time that the Asia-Pacific universe (where most of our exposure lies) is trading near its highest free cashflow yield since the GFC at some 5.7% vs. the S&P 500 at 2.7%. Twice the FCF yield at half the price, anyone?

But as you all know valuation alone is never a reason to buy a market. As the chart above shows the relative PE has been drifting for a number of years and yet this has not stopped the S&P showing EM a clean pair of heels since 2017.

Source: Aubrey Capital (Bloomberg) 28 February 2025

The direction of the USD is clearly the key to the appetite for EM equities. Whilst it appears at the top of its range on a number of metrics and has weakened of late who is to say it could not confound again at a time of geopolitical tension?

So, what could make a diversification into EM with its attractive relative valuation an auspicious move in the coming months?

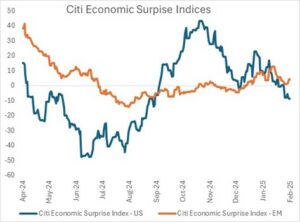

The Citi Economic Surprise index (CESI). The index plots the sum of the difference between actual official economic results and those forecasted. CESI results for the US and Emerging Markets may be worth a quick look. It appears that EM results have been surprising on the upside in a modest way while those for the US have been disappointing.

Source: Aubrey Capital (Bloomberg) 28 February 2025

The recent divergence of the chart above is a positive indicator for EM. The index for Emerging Markets when divided by the index for the US has been a good lead indicator of Emerging Market relative performance.

Source: Aubrey Capital (Bloomberg) 28 February 2025

As well as official macro announcements there also seem to be a number of factors which are more difficult to quantify: DeepSeek made investors question the huge capex budgets of the Magnificent 7 while positively reappraise China’s AI positioning (just look at Alibaba’s recent performance); meanwhile the Atlanta Fed has revised the US GDP forecast for Q1 to show a contraction at a 1.5% annual rate which will be the first quarterly contraction since 1Q22.

Timing is always a challenge. And one swallow has never made a summer but with the USD taking a breather and EM a nose so far this year is it time to at least think about diversifying.

Authors

Mark Martyrossian | Director, Head of Distribution

Mark joined Aubrey in 2017, having known Andrew Dalrymple for several years whilst working in Hong Kong together.

Since 1987, Mark has been involved with Asian equities in a number of capacities. This began in equity sales before he established and managed a trading book for Crosby Securities in Hong Kong. He was also responsible for initiating a corporate finance business focused primarily on China. After the sale of Crosby Securities, he joined Warburgs with his China team. On his return to London, Mark founded a FCA registered fund management business with a number of Asian equity strategies. He managed that business until 2016 when he sold his interest.

Read the full ‘The Great US Equity Party’ in PDF format.